What Is a Fed Rate Cut?

As the country's central bank, the Federal Reserve is responsible for guiding monetary policy, regulating the financial system and setting short-term interest rates. The Fed's main policy tool is its ability to adjust the fed funds rate, which is the interest rate that banks charge each other when they lend money overnight or for a few days. This rate serves as a benchmark for other interest rates paid by consumers and businesses.

"When the economy is expanding rapidly and inflation is soaring to levels in excess of 2%, the Fed will begin hiking rates as they did beginning in 2022," says Dwayne Safer, associate professor of finance at Messiah University in Mechanicsburg, Pennsylvania. However, "When economic conditions are slowing and unemployment is rising, the Fed typically begins lowering rates."

The Fed funds rate cut stimulates the economy by decreasing borrowing costs for consumers and businesses.

0.5% Rate Cut!

The Fed cut interest rates for the first time in years by half a percentage point on Wednesday in a move that experts predict will boost confidence and activity across the property market. Of the 12 Fed voters, 11 supported the cut, which will bring the benchmark federal-funds rate to a range between 4.75% and 5%.

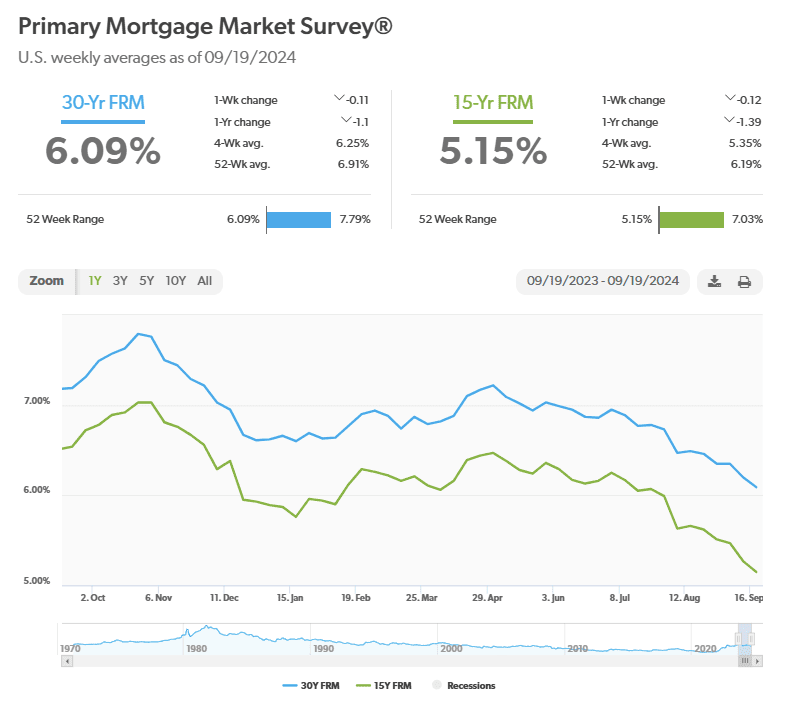

The effect of the adjustment and its impact on mortgage rates—will be felt most acutely across the middle and lower ends of the property market, where buyers rely on traditional financing for their home purchases. Mortgage rates started slipping ahead of the central bank’s Wednesday announcement, and as of Sept. 12 stood at 6.2%, the lowest since February 2023, according to lender Freddie Mac.

Buyers are massively affected by the sentiment of the market. If they see large numbers of contracts, people are more willing to pay up or pay faster.

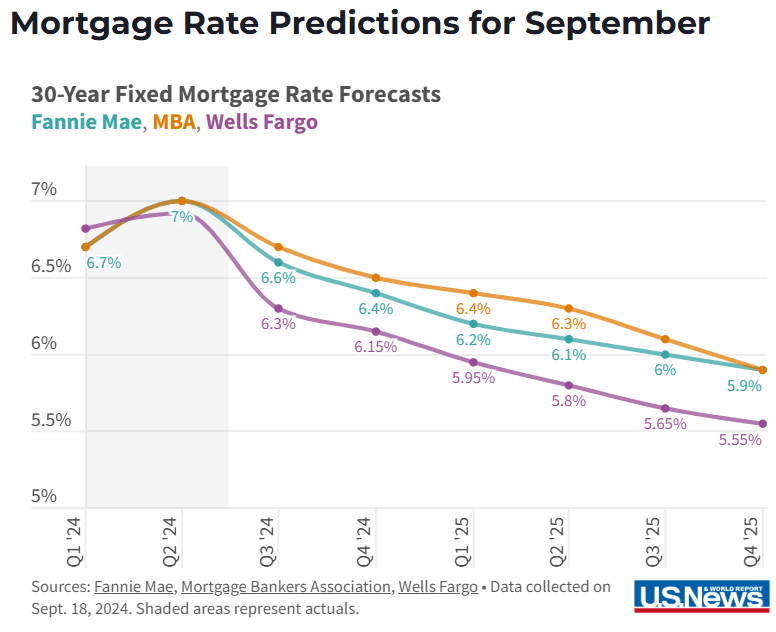

Mortgage rates have already declined by over half a percentage point (0.5%) between May and September. Mortgage rates should continue declining this year as the U.S. economy weakens, inflation cools and the Federal Reserve continues to cut interest rates. The 30-year fixed mortgage rate is expected to fall to the low-6% range through the end of 2024, dipping into high-5% territory in late 2025.

Official projections show the central bank will cut another 50 basis points this year (during their meetings on 11/6-7 and 12/17-18) and 100 basis points in 2025.

Advice for Buying or Selling a Home in 2024

Key Takeaways for Buyers

- Mortgage rates are expected to decline somewhat in 2024, but not drastically

- Those who are waiting for mortgage rates to drop before buying a house will likely be on the sidelines while home prices continue to appreciate, and falling rates could push prices even higher.

- It makes sense to buy a home now if you can comfortably afford the monthly payments and you can cover the cost of maintenance, property taxes and other homeownership expenses.

- Lower Rates Could Spark Competition – and Drive Prices Higher

What Buyers Should Know: Home Prices Won't Come Crashing Down

Good things may come to those who wait, but patience doesn't always pay off in the housing market. Two-thirds of homebuyers are waiting for mortgage rates to fall this year before buying a home, according to a March U.S. News survey. The vast majority of them (85%) wanted to see rates below 6% before entering the market, which hasn't happened – and it isn't expected to happen until 2025.

One factor is the rate lock-in effect, where many homeowners are reluctant to list their homes for sale since they have much lower interest rates (and monthly payments) than what's currently available. About four in five homeowners have a mortgage rate below 5%, according to a January 2024 study by the online real estate brokerage Redfin. That reluctance to sell causes a decline in housing inventory.

If mortgage rates do fall this year, some homeowners could be motivated to sell, but the vast majority will still have much lower rates than what's currently available for the foreseeable future. At the same time, first-time buyers might decide to enter the market if rates fall even slightly, unleashing a wave of pent-up demand that could outweigh the relative improvement in supply.

If a buyer want to beat the competition and is financially capable, buying now and re-financing later is the best course of action.

If buyers are holding out for lower rates, home prices will continue to rise and buyers could see themselves priced out of the market.

"Strong home price appreciation has persisted despite purchase affordability remaining stretched for the vast majority of consumers, a dynamic that is still primarily a function of inadequate supply," says Mark Palim, Fannie Mae's vice president and deputy chief economist, in a Sept. 5 statement.

Even the most seasoned economists have trouble predicting mortgage rate trends, so the average homebuyer has little chance of successfully timing the market. Instead, buyers should focus on things within their control, like deciding what they want out of a home and working with a real estate agent to put in a competitive purchase offer.

What Sellers Should Know: Remember That You're a Buyer, Too

Perhaps the biggest hurdle facing sellers is that they still need a place to live once they've sold their current home. For many, that means overcoming the lock-in gap to buy a new home at today's rates and home prices.

However, there is a silver lining for sellers who are also buyers: Most homeowners who have been at their current home for at least a few years are sitting on a mountain of equity thanks to double-digit home price appreciation during that time. With a successful sale, homeowners can tap into that equity to put toward their next home purchase.

According to Federal Housing Finance Agency data, the average interest rate on existing mortgages is 4.1% – far lower than the current prevailing rate available to new homebuyers. In fact, 86% of homeowners have a rate below 6%, and rates aren't expected to dip below that threshold this year.

Alternatively, sellers that chose to wait may face unexpected sudden home repairs costs, like roof or mechanicals, that can be very costly. In addition, lifestyle changes, a new job or simply impatience having endured high rates for the past 2 years may cause homeowners to move.