A Brighter 2024 Ahead

End-of-Year Recap 2023: The "Bottom-Out" Year

Real Estate is hyper-local, especially in this market! With inflation dropping and inventory still low in Northern New Jersey, if you are even remotely thinking about selling or buying a home, now is the time, before the market gets crazy with competition. Especially because of the projected rate cuts in 2024, there will be a frenzy before you know it.

Here are some facts and statistics:

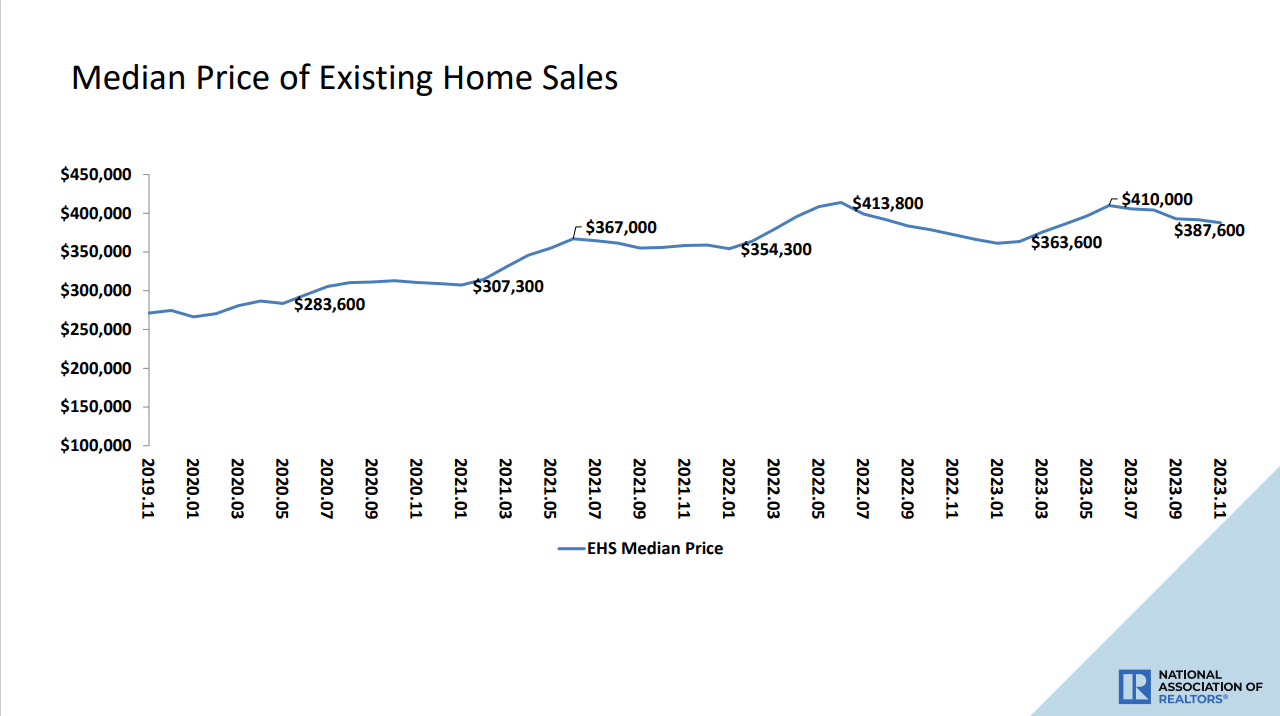

Nationally: On a national level, the median home prices have been declining since June 2023.

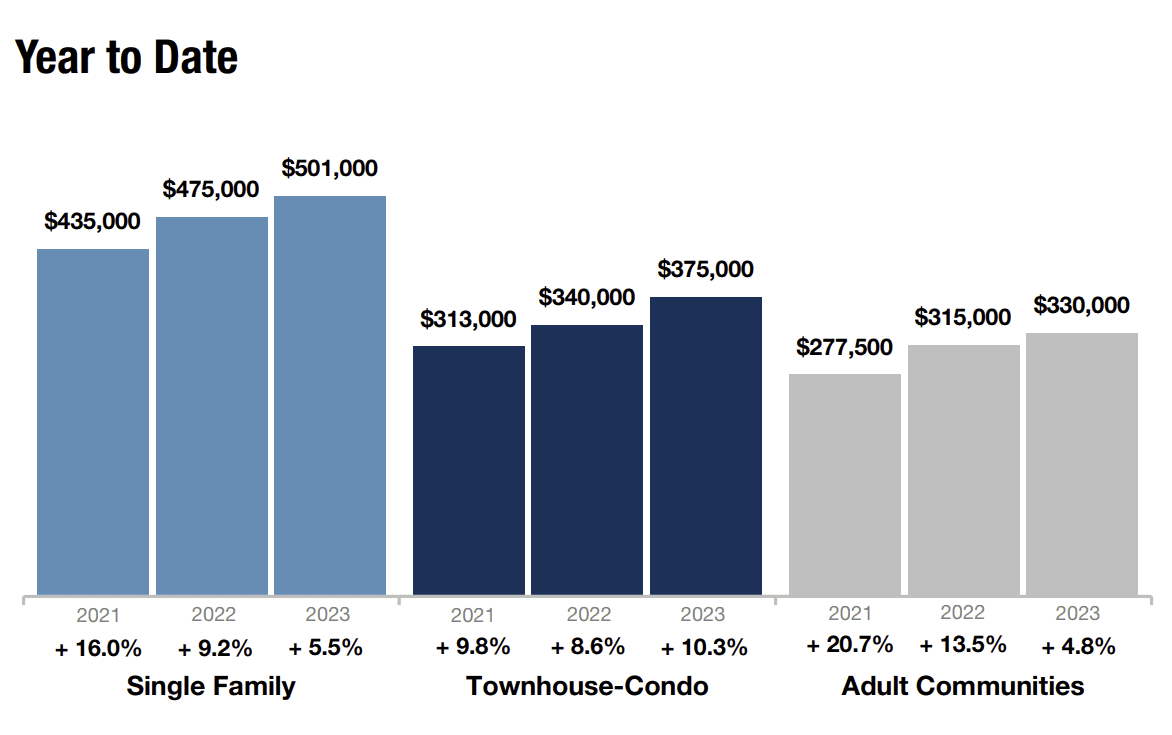

New Jersey: However, Northern NJ has been stronger than ever with a steadily rising Median Sales Price

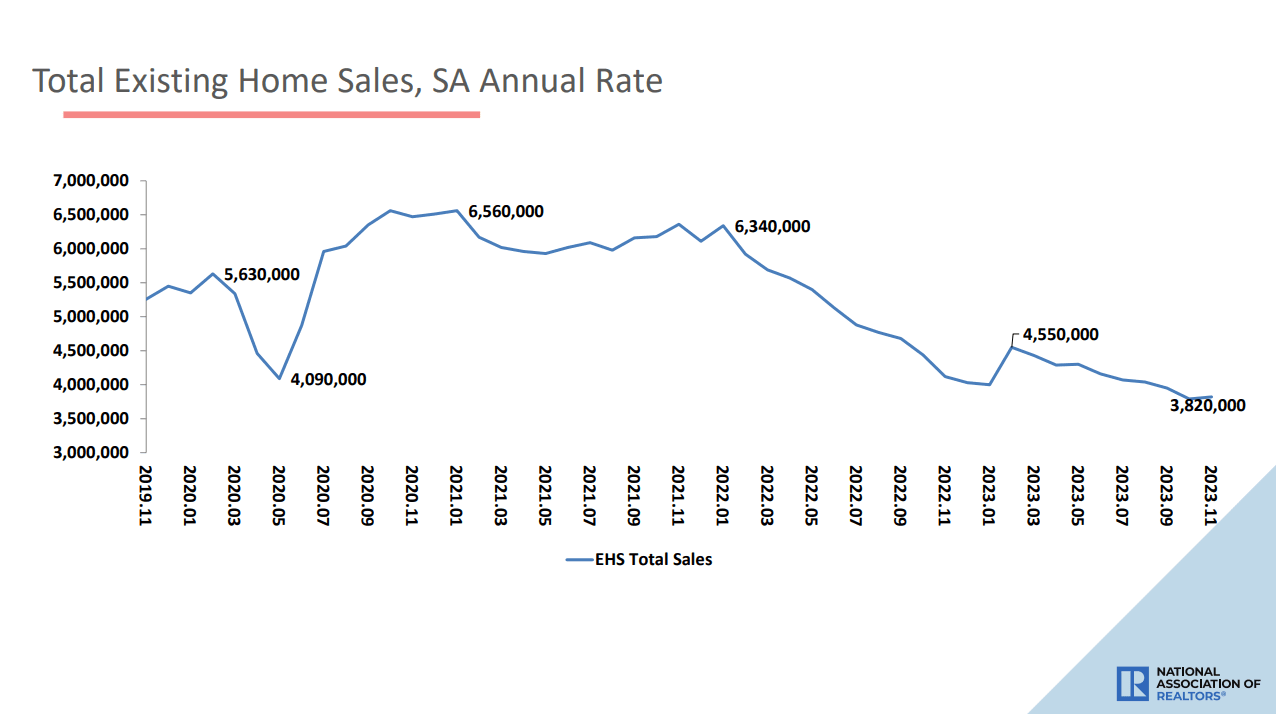

Since 2021 fewer and fewer home sales have been recorded year over year. This has created a backlog of home buyers and pent-up housing demand.

As the inventory is still tight, NJ has 70% fewer homes on the market compared to pre-pandemic levels in 2019 while purchase contracts are “only” down by about 30%. That shows that high interest rates did not have buyers shy away from home purchases - the lack of inventory did.

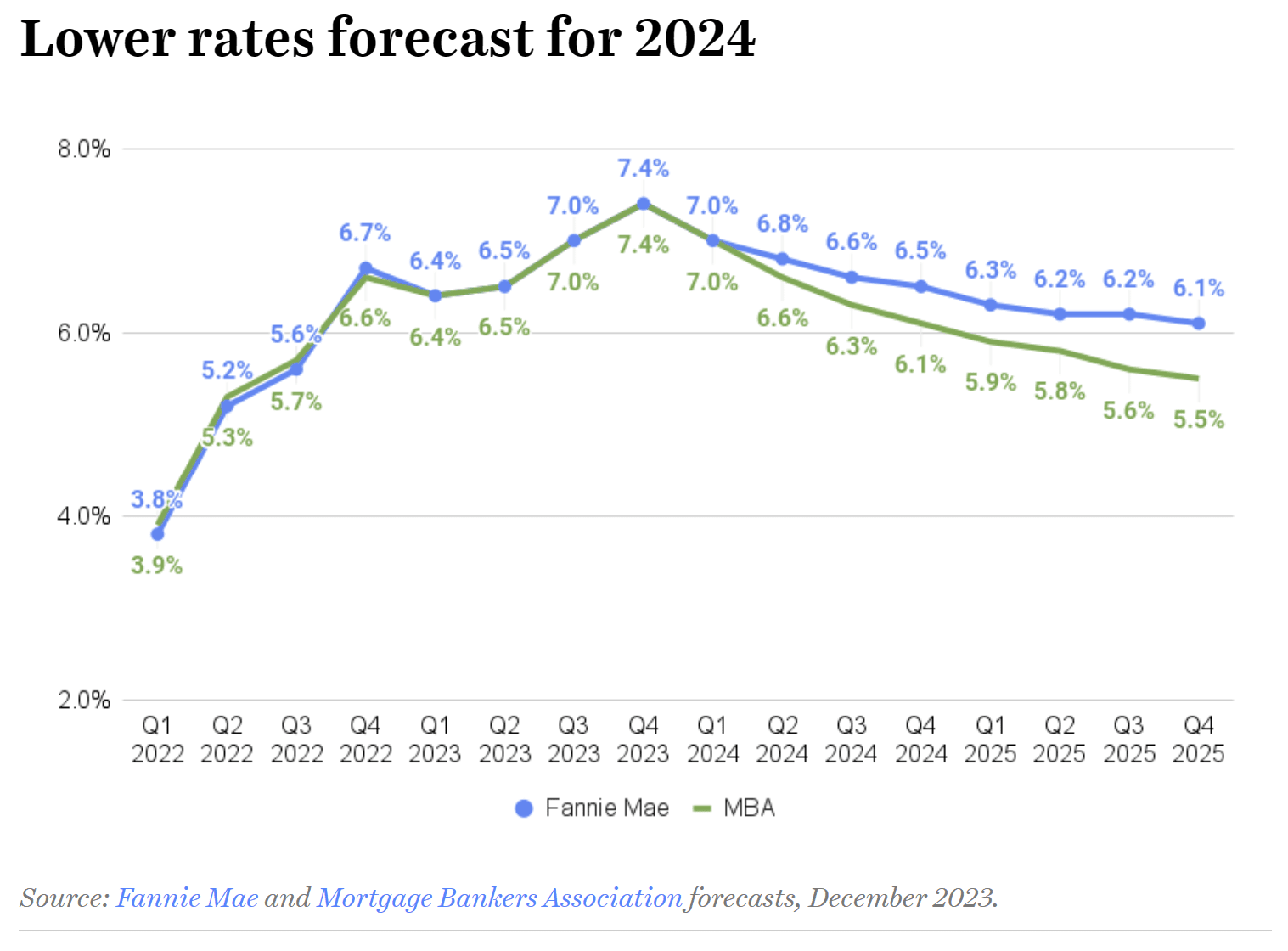

The expected growth in home sales in 2024, coupled with continued but slower growth in home prices, could boost 2024 purchase mortgage volume by 14 percent, MBA forecasters predict. And if mortgage rates fall as quickly as they envision, MBA economists see refinancing volume bouncing back by 56 percent next year.

The Early Bird Will Catch The Worm in 2024!

INFLATION - Dropping Faster Than Expected

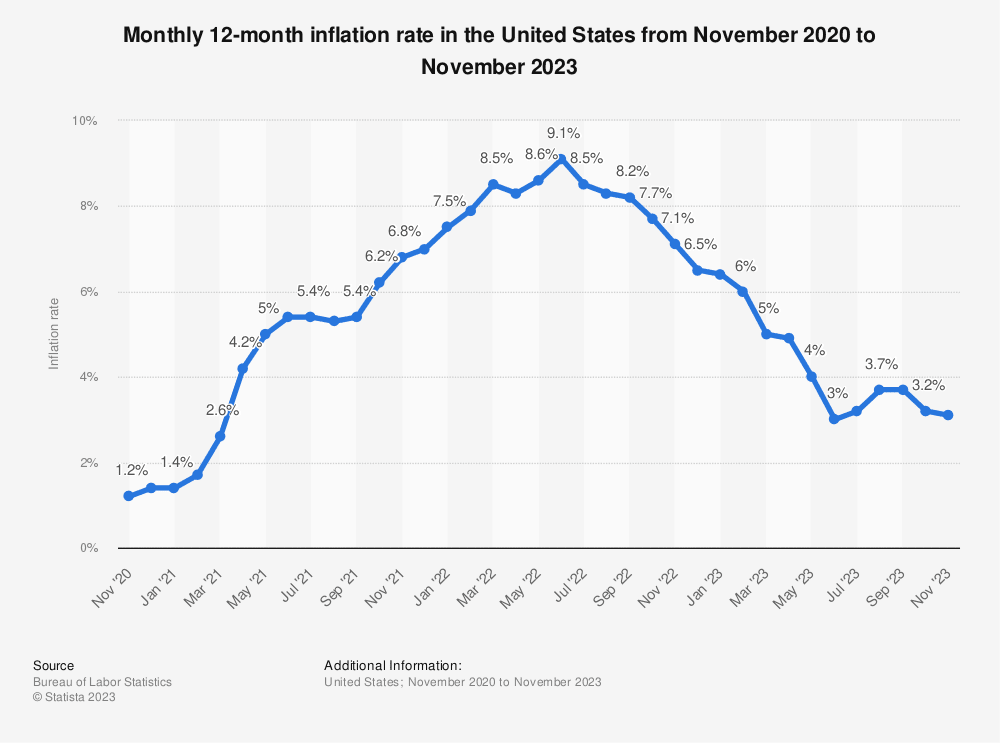

Inflation in the US rose to 9.1%, peaking in June 2022. Over the past 18 months the rate has steadily dropped to 3.1% today and is expected to reach the targeted 2% level much sooner than officials expected.

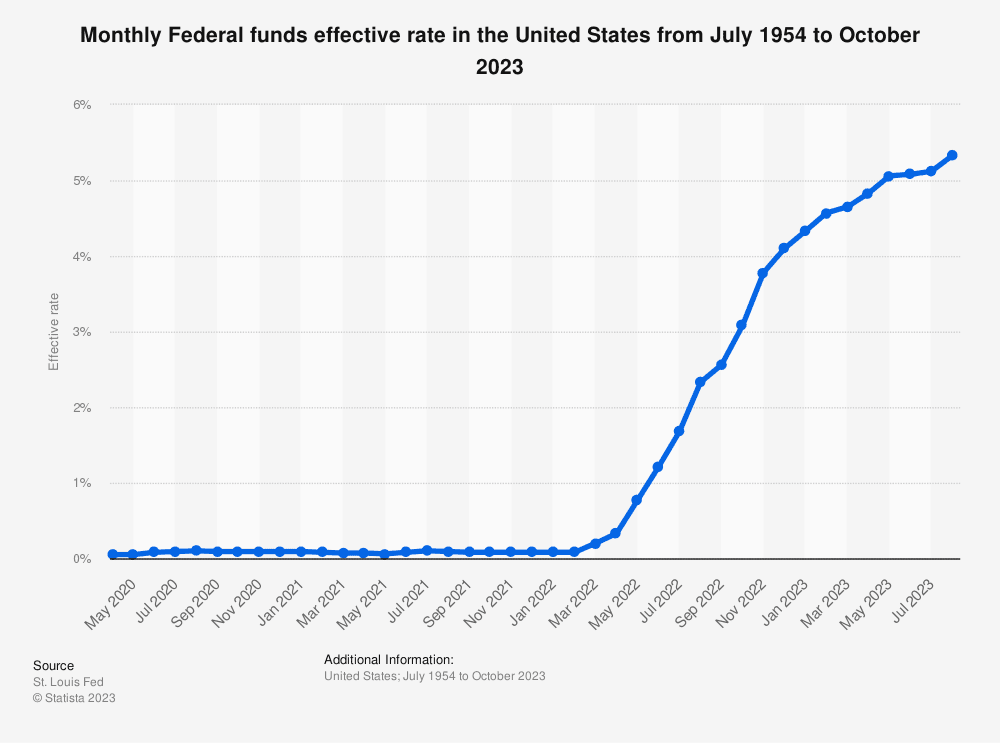

FEDERAL FUNDS RATE - Unchanged Since September 2023

Most projections show expectations for 3 - 6 rate cuts in 2024.

Starting in May 2022, as a response to the rising inflation, the FED increased the rate 11 times between May 2022 and July 2023. As of October 2023, the rate is at a level of 5.33%.

Economists say that with inflation hitting a new recent low around 3% in December 2023, the FED should be encouraged to leave the interest rates unchanged for now. They already held steady since September 2023 - during the last 3 meetings on 9/20, 11/1 and 12/13.

Officials expect inflation to reach their target of 2% sooner than expected. The FED meets about every 6 weeks, 8 times a year, with the next meeting scheduled on 1/31/2024.

Most projections showed expectations for 3 - 6 rate cuts in 2024.

What is the Federal Funds Effective Rate?

The U.S. federal funds effective rate determines the interest rate paid by depository institutions, such as banks and credit unions, that lend reserve balances to other depository institutions overnight.

Changing the effective rate in times of crisis is a common way to stimulate the economy, as it has a significant impact on the whole economy, such as economic growth, employment, and inflation. As a response to the COVID-19 pandemic, the U.S. federal funds effective rate was drastically lowered between February and April 2020 - it was set at 0.33 percent in April 2022 to stimulate the economy. Most projections showed expectations for 3 - 6 rate cuts in 2024.

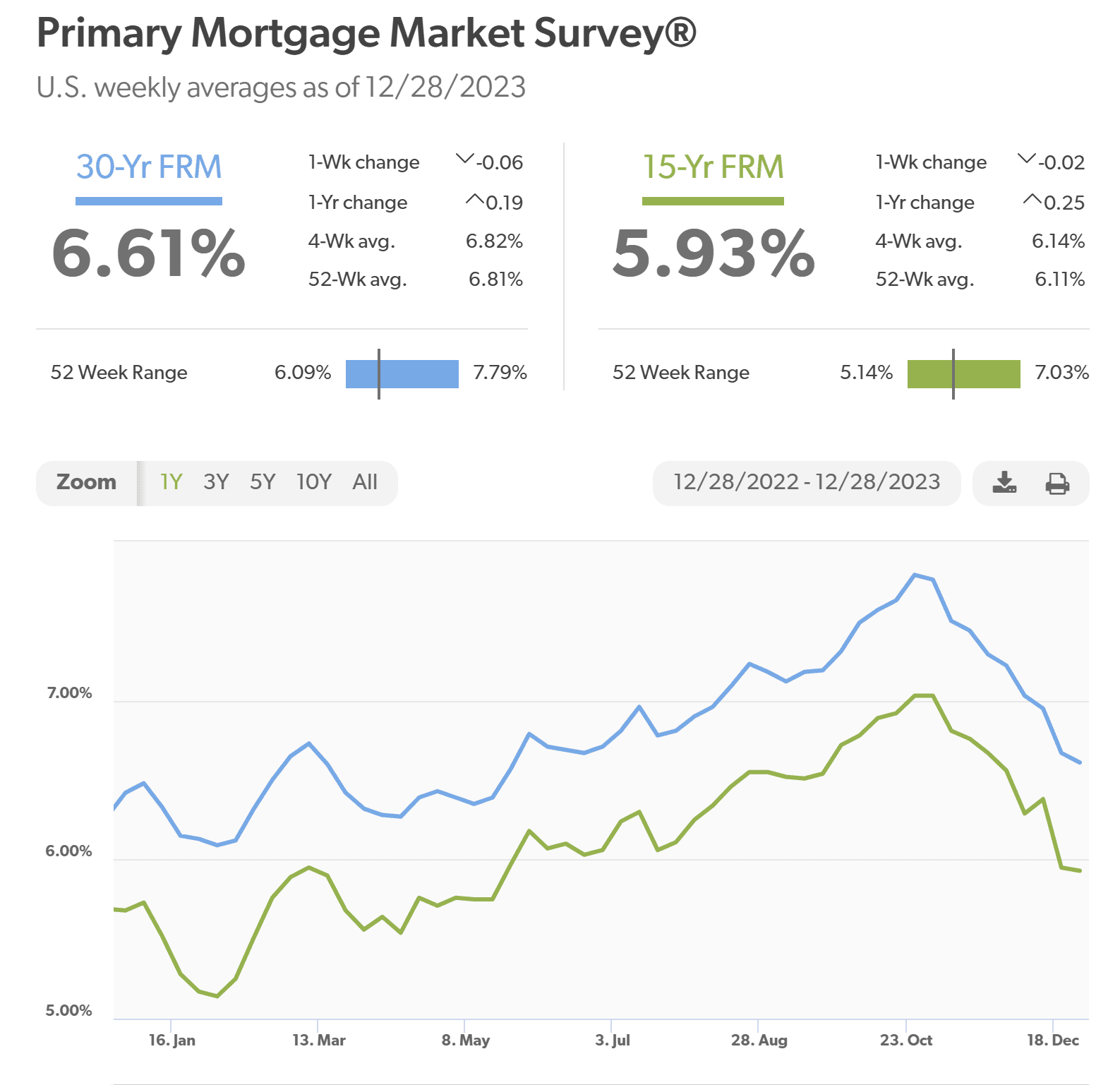

MORTGAGE RATES - Have Been Dropping Since Late October

Mortgage Bankers Association (MBA) and Fannie Mae economists agree (this time!) that on a national level home sales probably bottomed out in Q4 2023, and forecasters at both organizations now expect to see mortgage rates come down significantly next year re-fueling again the housing market.

If rate cuts are expected, should you wait to sell or buy?

Not really...

Mortgage rates move based on demand for mortgage-backed securities, and investors typically act in anticipation of Fed actions. Since late October, mortgage rates dropped for the 5th consecutive week by about 0.75%-points, giving buyers the opportunity to access lower rates before the Fed makes a move.

Mortgage rates started to climb in April 2022 as a response to the end of the pandemic coupled with the start of rising inflation. Over a period of 18 months, rates moved up by about 500 basis points (5%-points) from the high 2% to the high 7% in late October 2023. Since late October mortgage rates are on a decline and now in the low to mid 6%.

That means that in today’s market lower mortgage rates are almost a precursor for future FED rate cuts. Lower overnight rates will stimulate the economy, resulting in higher GDP and lower unemployment over time. By the time that those statistics are reported, the housing market is again in full swing, this time with a backlog of buyers since pre-covid times - meaning a 4-year backlog of buyers. Most sellers are also again buyers … so as a buyer or as a seller you want to come to the market early to beat the crowd.

Mortgage Rates - Freddie Mac

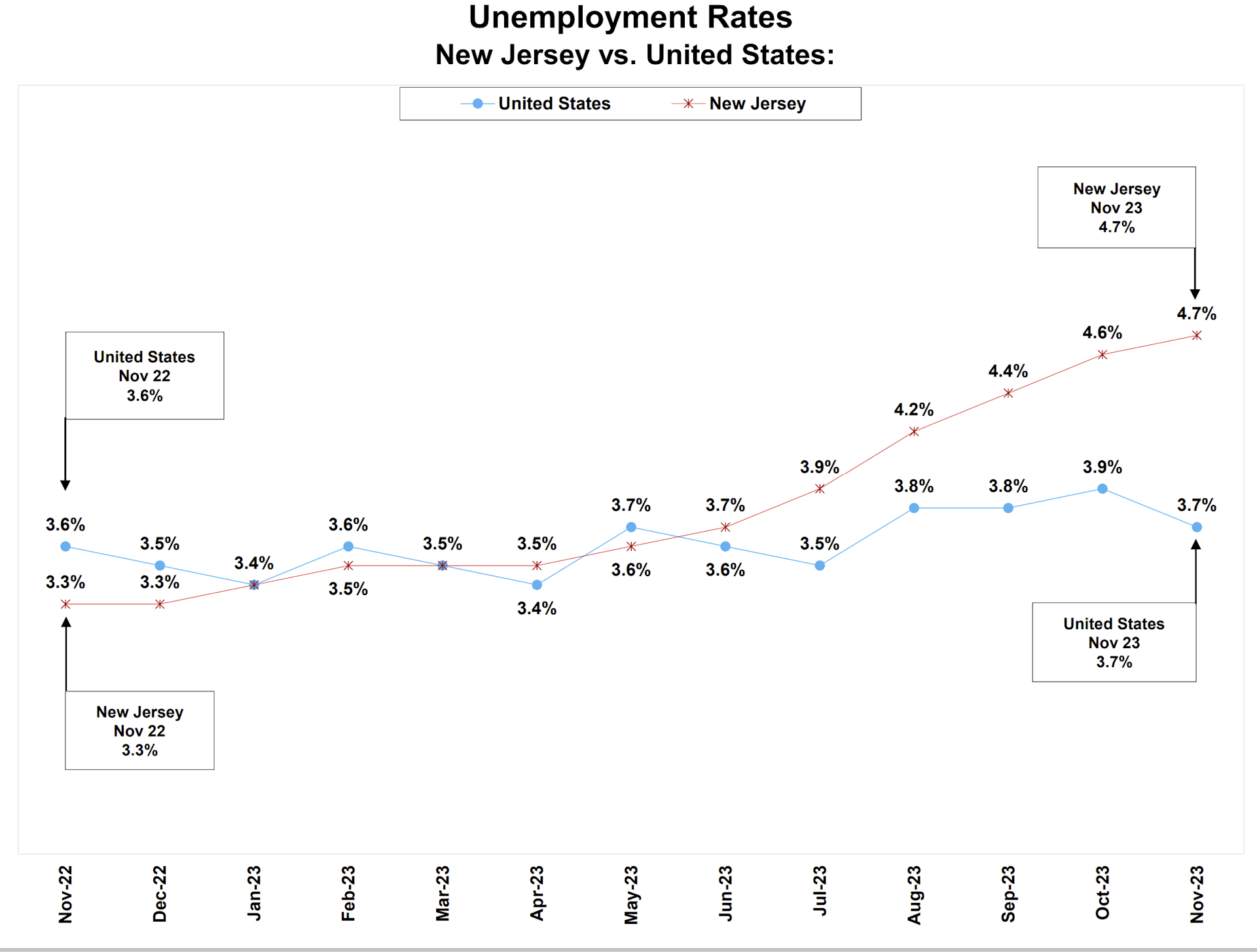

UNEMPLOYMENT

During the height of the pandemic the highest unemployment rate in the US was 8% - and in NJ it almost reached 16%. As the economy softens, NJ has now the 4th highest unemployment in the country with 4.6% compared to a national average of 3.7% in November 2023. However, this will not have an adverse effect on the housing market going forward as rate cuts and lower interest rates will stimulate the economy again in 2024.